Crypto Tax in Portugal

Last updated: 10 February 2026

El Dorado, the golden kingdom. A mythical place of inestimable value where, according to legend, everything was made of gold.

For many years, Portugal was El Dorado for crypto investors. Inestimable value was certainly created there too. Inestimable primarily because I'm talking about crypto assets. And for a long, long time, these were completely ignored by the Portuguese tax authorities.

Why?

The Portuguese tax office didn't fail to tax them on purpose. It wasn't an intentional benefit or an official government programme.

Unlike the NHR regime in Portugal.

No, it was yet another unintentional loophole. Technological progress simply outpaced the lawmakers and the tax administration.

Crypto assets were not included on the official list of taxable capital assets.

And only gains from the disposal of assets specifically on that list could be taxed as "Capital Gains" or investment income.

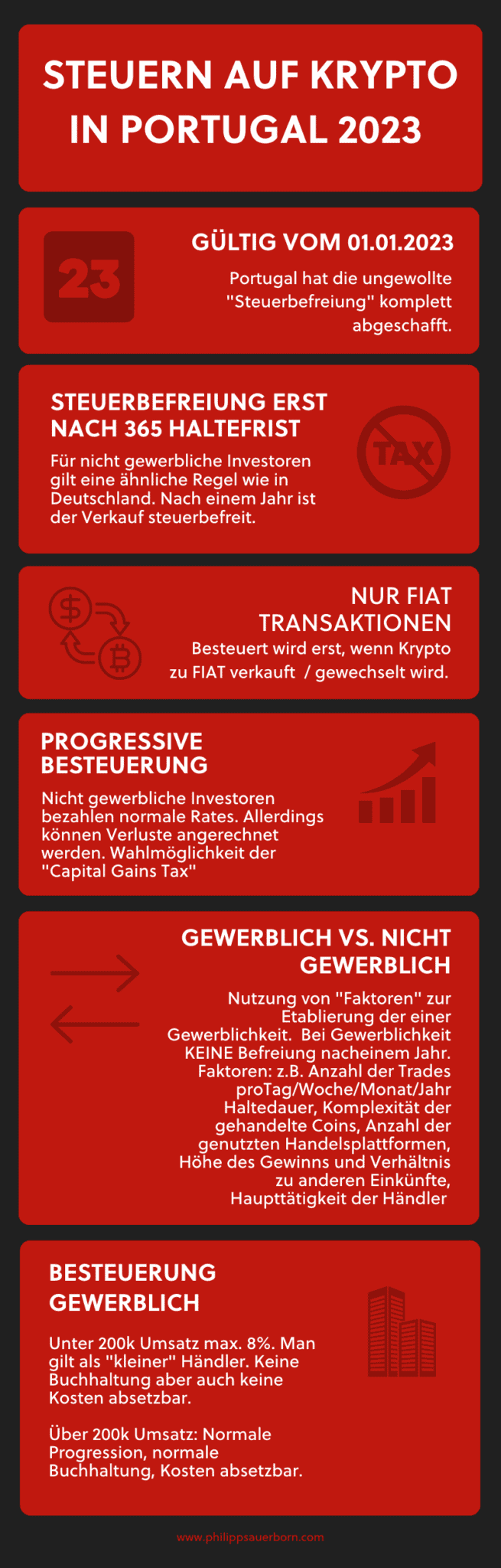

That's why Portugal was the crypto El Dorado. Pretty much exactly until 1 January 2023.

Because in 2023, everything changed. Incidentally, nothing changed for professional traders—they were and still are taxed like any other business. However, there are new regulations regarding how that "commercial" tax is calculated.

This means the changes really only affect "investors" who aren't selling crypto commercially.

I'll get to the details of that in a moment.

Huge Disclaimer: The following information applies exclusively to NON-COMMERCIAL investors. And while we're disclaiming: Tokens or coins that classify as SECURITIES are NOT covered by this new rule either.

A thin fine line:

Both disclaimers remain one of the main issues with crypto, both in terms of tax law and regulation.

Therefore:

It is best to get advice on exactly how your crypto portfolio—or parts of it—are classified.

But now, let's look at the new 2023 tax rules for crypto in Portugal.

The Holding Period

The Portuguese simply copied this from the Germans—100%. If you hold crypto for 365 days, i.e., for a year or longer, the exemption still applies, and you pay no tax.

Note to self: Gains after a 365-day holding period equal zero tax in Portugal.

Selling within 365 days

If you buy and sell within 365 days, you make either a profit or a loss. Both are taxable events in Portugal. Taxable means gains must be taxed, and losses can be carried forward and offset for a maximum of 5 years.

That's actually not too bad. However, it only works if you use the normal progressive tax rates in Portugal.

Which are as follows:

| Income | Tax Rate Portugal (2025) |

|---|---|

| 0 – €8,059 | 12.5% |

| €8,059–€12,160 | 16% |

| €12,160–€17,233 | 21.5% |

| €17,233–€22,306 | 24.4% |

| €22,306–€28,400 | 31.4% |

| €28,400–€41,629 | 34.9% |

| €41,629–€44,987 | 43.1% |

| €44,987–€83,696 | 44.6% |

| Above €83,696 | 48% |

Mind you, these rates don't apply separately; they are added to any other income you have. That means if you already earn €40k a year from a job, for example, you start taxing your crypto gains at the €40k bracket, not at zero.

Of course, as with any tax return, you must ensure you can provide robust documentation of the transaction in question. Specifically, when you bought and when you sold. Crypto exchanges usually provide this.

If you buy or sell OTC or directly (e.g., Local Bitcoin), proper documentation must accompany the transaction there too.

You can ignore Crypto-to-Crypto trades.

Because: Portugal only taxes transactions to FIAT.

Gains on pure crypto trades are "deferred" until the gain is eventually realized, in whole or in part, into FIAT currency.

Two important notes for crypto taxes in Portugal:

- Losses are only accepted if they arise from transactions with countries that are not "blacklisted." So, if you think you're being clever by asking a buddy in an offshore jurisdiction for an invoice, you need to know that this transaction will NOT be recognized for LOSSES.

- If you live in Portugal and only trade crypto-to-crypto, you have no tax to pay, as mentioned above. However, if you then want to leave Portugal, a fictitious sale to FIAT will be assumed for tax purposes (Exit Tax), unless you are moving within the EU.

Choosing the Capital Gains Tax

Taxation according to the Portuguese progressive income tax rates mentioned above is optional. You can also choose to be taxed at a flat 28% on the actual "Capital Gains." This makes sense if your other income already pushes you into a higher tax bracket.

However:

If you opt for this flat rate taxation, you cannot offset losses.

Staking and Off-Chain Investment in Portugal

For "passive" income in FIAT generated through crypto, you cannot choose the progressive rate. This means the Capital Gains Tax of 28% applies to any positive "interest income."

By "passive," I mean income generated without moving or trading the crypto.

Commercial Crypto Trading in Portugal

For me, this is a genuinely innovative way of taxation. I'll get to the "how" and "how much" in a moment. Much more important, however, is the question of "IF."

Am I a professional trader or not?

This question has kept tax advisors and tax officers busy for centuries. Unfortunately, there is no clear-cut answer. In Portugal, you can be considered commercial regardless of the holding period.

What makes you a "Professional"?

In international tax law, there is a tool—a framework. I'm talking about the "Badges of Trade." You could also call them indicators of a business.

The problem with these indicators is that one, several, or all of them can "identify" a business. That means it's always a matter of how you present yourself, but also a question of interpretation.

The tax administration in Portugal also uses Badges of Trade. As far as I know, they call them "factors" in Portugal.

Portugal IRS Factors for Commercial / Professional Crypto

- Number of trades per day/week/month/year.

- Holding period of financial products

- Complexity of traded financial products

- Number of trading platforms used

- Debt-to-equity ratio, credit financing

- Profit level and relationship to other income

- Additional relevant trading activities (such as advice)

- Traders’ main activity (where else do you get your money from?)

The "Real" or "Original" Badges of Trade

It certainly can't hurt to take a look at the "original" Badges of Trade. I find this ACCA article to be by far the best on the subject:

It contains the 9 badges along with extensive explanations. I'll just list the badges in bullets here; check out the link if you have the time and inclination.

ACCA Badges of Trade

- Profit-seeking motive

- The number of transactions

- The nature of the asset

- Existence of similar trading transactions or interests

- Changes to the asset

- The way the sale was carried out

- The source of finance

- Interval of time between purchase and sale

- Method of acquisition

There are obviously many parallels here with the "factors" used by the IRS in Portugal.

Be that as it may:

A completely different modus operandi applies if you are taxed as a "Business" or "Professional." And as I wrote above, this is actually something new.

A business actually pays significantly less tax.

The New Taxation for Crypto Business / Commercial / Professionals

Up to €200,000 Gross Profit

First, a distinction is made between the big players and the small ones, based on turnover. But it's not trading volume that counts as turnover, but the actual gross profit from trading or mining.

Let's start with trading—what constitutes gross profit?

Revenue from Crypto Trading in Portugal

Simply put: Crypto Sales minus Crypto Purchases. Up to a delta of €200k, you are considered small.

As soon as you are no longer considered "small," you do what any business is expected to do.

Accounting, turnover, costs, receipts, bank statements, etc. You have to do standard bookkeeping.

The "small" players have it easier. No bookkeeping is required. A coefficient is applied: 15% of the revenue is taken as the taxable base for professional "small" traders. Costs are not taken into account. The progressive tax rate is then applied to that 15%. Effectively, you pay a maximum of 8%. Now that is a statement.

A quick calculation example:

Let's assume you are already in the highest tax bracket in Portugal and pay 48% there. You show crypto revenue of €200k. We take 15% of that. That's €30,000 of taxable income. So you pay €14,400 in taxes (48% of the €30k). But measured against the €200k net profit, it's just roughly 7-8%.

Revenue from Mining

For mining, however, 95% is taxed instead of 15%. Otherwise, the calculation is exactly the same as for trading.

Interim Conclusion: Portugal has closed the crypto loophole. The new regulations aren't the end of the world, but things could definitely be better. The taxes, and above all the risk of falling into the "commercial trading" trap, are unpleasant.

So what can you do?

My advice: Get rid of the sword of Damocles that is the "commercial risk" and simply accept the commercial status. But don't open the business in Portugal. Instead:

Form a Malta Limited for Crypto Trading in Portugal.

It gets even better if you aren't yet benefiting from the NHR or its successor, the IFICI regime. Because NHR/IFICI in Portugal doesn't really work directly for crypto.

Here is the play:

Company Formation in Malta with Portugal NHR/IFICI Regime for Crypto Income.

Let me explain briefly:

Under the Portugal NHR regime (replaced by IFICI since 2024, but with similar benefits for foreign dividends), foreign dividends are exempt from tax in Portugal. And in Malta, you pay significantly less tax than in Portugal. Plus, with the Ltd, you are on "Blockchain Island," because Malta is crypto-friendly.

With the right structure and the right advice, you can live in Portugal and trade your crypto via the Malta Limited: Commercial, official, registered, and you pay an effective tax rate of just 5% in Malta.

Sounds good to me.

Sounds like El Dorado.

Disclaimer: The content of this article is for general information purposes only and does not constitute tax, legal or financial advice. Despite careful research, we make no guarantee for the accuracy, completeness and timeliness of the information provided. Tax regulations are subject to constant change. For individual advice, please consult a qualified tax advisor. Use of the content is at your own risk.

Stay Informed

Receive our latest articles on international tax planning, relocation and company formation directly in your inbox.

No spam. Unsubscribe anytime.