Malta Limited with UK Residence vs. Malta Residence: 10 Rules You Must Follow

Last updated: 1 March 2026

First, let me be clear:

This article focuses primarily on tax aspects.

I'm not asking the question of whether you could move to Malta at all. I know that for many, this simply isn't an option due to personal or family reasons. In plain English:

Not all the reasons and situations I describe here apply to everyone, because for some, moving to Malta is simply off the table.

However, for the sake of simplicity, let's assume that personal reasons aren't holding you back and make the following assumptions:

- You are thinking about a change of scenery anyway

- Your business can be managed from anywhere

- You basically like Malta

Nevertheless, you want to know if the move to Malta is the right path. This brings us to the core questions this article addresses:

What do I need to watch out for? What is the difference if I run a Malta Limited from the UK, versus running it from Malta, while living in Malta?

I will provide you with well-founded answers to this.

If you are already a step further and just have two questions:

- Is a company worth it for me? and

- Can this be implemented legally with my specific business case?

...then the DWP QuickCheck is exactly the right tool for you. Free of charge and in just 5 minutes, you can test whether your business is suitable for this location.

CHAPTER 1

Residence Counts: How You Trigger Tax Residence in the UK

You can be as convinced as you like that you live in Malta…

…in the end, HMRC has to agree with you.

There are specific rules that create a clear presumption:

Your residence is in the UK.

I'll explain which ones.

The shareholder's residence is decisive for the applicable tax law

In my article on forming a Malta Limited, I briefly touched on this:

Everyone wants their fair share. Including the tax authorities.

Consequently, you are a tax resident where you live.

Makes sense.

For our example of the UK, this means: If you are considered a resident under the Statutory Residence Test (SRT) or maintain your primary home there, you clearly fall under UK tax legislation.

So, you are liable for tax on your worldwide income in the UK (unless you are a non-dom claiming the remittance basis, but that's a different story). Whether you like it or not.

There are several indicators that suggest you are resident in the UK. I'm not saying these are THE deciding points—that varies, as I always say, from case to case.

But from my experience, I can say that these points often play a major role.

Do some of the following apply to you?

Shareholder Residence: What to Watch Out for with HMRC

The shareholder's residence is of interest primarily to one party…

…HMRC (His Majesty's Revenue and Customs).

There are several points that must be observed here. And believe me:

The authorities work well and precisely! Therefore: Please pay attention.

UK Residence: Tax Liability Means More Than Just Paying Taxes

At the start of this chapter, a question:

What does tax liability with a UK residence mean to you?

Well, the heading gives it away a bit. At the very least, it's not just that you have to pay taxes. No, the consequences are significantly larger. For example, the UK government can dictate all the rules that apply to a taxpayer there.

This applies particularly to shareholders of companies abroad who live in the UK. Because the legislator makes a basic assumption:

Anyone who wants to start a company does so in their home country.

In my eyes, this assumption is completely justified. After all, the UK offers the right infrastructure for any venture. This basic assumption simultaneously leads to a fundamental doubt if the incorporation did not take place in the UK.

So, if you decide against the UK, the consequence is that you must have plausible reasons for doing so. And…

…you must be able to prove them and subsequently adhere to various rules and conditions.

By the way: You might think that a tax burden that seems too high represents a valid reason. That is not the case!

Tax Defense: The UK Protects Its Tax Revenue, Even from Malta Shareholders

Another point to note regarding the UK is a certain tax defensiveness. It is the job of the UK government to protect its tax base.

Believe me: The state does not do this with any malicious intent.

Rather, in my view, it is justified and common practice in international tax policy. Because it's clear: If someone lives and works in the UK, they should also make their contribution.

Nevertheless, there are valid reasons for setting up a company abroad, such as forming a Malta Limited. But no matter how and with what intention you found a company abroad, you must be prepared for one thing:

Protective mechanisms provided for in UK tax law can kick in to prevent profits from being "shifted" to lower-taxed countries.

Clearly, these mechanisms are primarily intended to filter out the "bad guys," but like any precautionary measure, they also affect those who incorporate abroad with the best intentions. You have to get used to the fact that your corporate structure will be questioned and scrutinized.

I will shed light on these protective mechanisms in a moment, and then compare them to show exactly where the differences lie if you, as a shareholder of a Malta Limited, live in the UK versus living in Malta.

The Most Important Rules for Foreign Companies: CFC Rules

What exists in German tax law as the "Außensteuergesetz" is known internationally—and in the UK—as CFC Rules (Controlled Foreign Company Rules). Of course, there are significant differences from country to country, but usually, the same thing happens if you don't stick to the rules I'm about to present:

The relevant tax authority looks "through" the company in Malta. What does that mean? Quite simply: All profits are attributed directly and personally to the shareholder, as if they had set up a sole proprietorship in their home country.

Therefore: Anyone living in the UK who is a shareholder of a company in Malta should urgently adhere to the following 10 Commandments.

Then take advantage of a free and non-binding consultation with me. Simply write me a message in the contact form and I will get back to you promptly.

[Contact Me]

CHAPTER 2

10 Commandments You Must Follow as a Foreign Shareholder Residing in the UK

Here they are…

…the 10 Commandments you must observe as a shareholder of a company abroad with UK residence.

A long sentence with a clear essence: You should urgently follow these rules!

Let's get to the heart of the matter.

A small note at the beginning: These rules are particularly relevant when the shareholder holds a significant interest in the Malta Limited. The specific thresholds vary by rule (e.g., UK CFC rules look at control, typically more than 50%, while reporting obligations can apply at lower levels).

1. Every Shareholding Must Be Reported

If you are a shareholder of a company in Malta, you must report this. And do so immediately. There is no point in trying to cover it up. Keyword: CRS (Common Reporting Standard).

Once a year, non-resident citizens are reported to their domestic tax authority anyway. That is why every bank requires your UTR (Unique Taxpayer Reference) or National Insurance number when opening an account.

2. Shareholders Must Show a Valid Economic Reason (Principal Purpose)

Even though freedom of establishment in the EU is one of the highest goods (and relevant for Malta), there must be valid economic reasons for the company that justify incorporation in Malta.

Again, the note: High taxes at home are not accepted as a valid reason. The reason must exist independently of tax.

A tip: The often-cited reason of "internationalisation" is long known to tax authorities. If you cite this but then mainly serve UK customers, you won't get away with it.

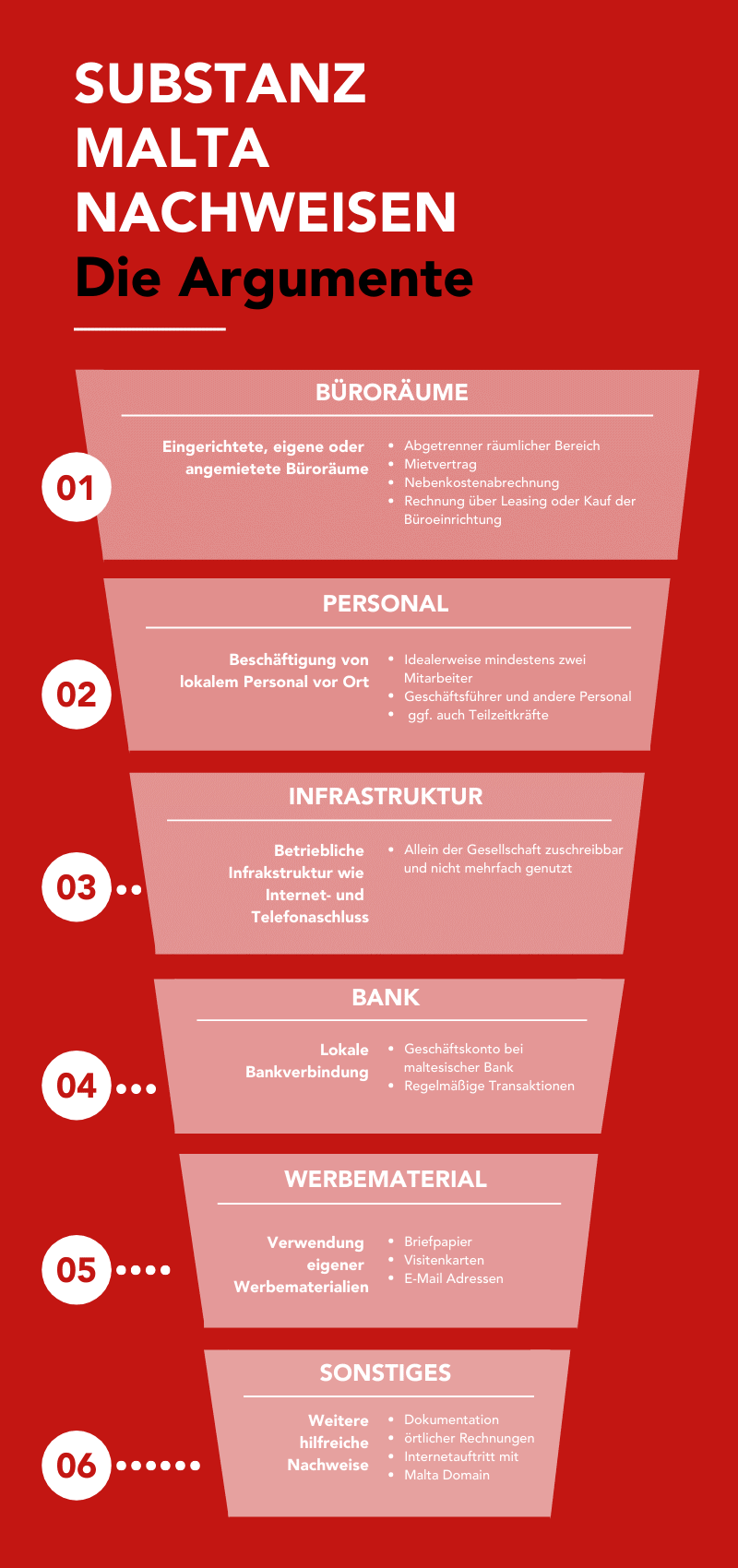

3. The Malta Limited Must Show Sufficient Substance

I explained this point in detail in my Guide to Company Formation in Malta, so just briefly:

Even though the possibilities here differ depending on the business case, certain things should be implemented to prove the substance of the company in Malta. Therefore, below is an infographic with possibilities for building substance, which we at Dr. Werner & Partners interpret as the minimum (ordered by priority).

4. Management of the Malta Limited is in Malta

An important point is the place of management of the company. Although this point has lost some of its status over the years, it still applies:

For determining the residence of the company, the place of central management and control is a central element.

How is this checked? Good question!

HMRC tests whether the company is legitimately managed "in and from" Malta. Usually, a letter is sent to the company's address asking, among other things, the following questions:

- Who is the director of the Malta Limited?

- Where does the director reside?

- Since when has the director been leading the Malta Limited?

- What is the director's income?

- How many companies is the director registered with?

- Is the director a professional provider such as a lawyer, trustee, or tax advisor?

In addition, the tax office then requests some evidence:

- The director's employment contract

- Proof of social security payments in Malta

- Proof of salary payment

- Proof of the director's qualifications

- Proof of work activity on site

Some of you will certainly have heard of the "Rubberstamp Policy" in this context. This involved providing valid proof of activities simply by a stamp or a signature from Malta. Let me tell you: Those days are over.

Another small note on the subject of salary: Staff in Malta must always be paid adequately. That means:

If a director of an international company earns only £1,000 a month, that seems implausible.

There is no clear minimum or maximum here; market-rate payment is the keyword. To check, simply ask yourself the question:

What would a third party earn if I acquired them on the open market and hired them as a director?

5. Transfer of Assets and Corporate Exit Charges

A very sensitive topic: Transferring assets.

If you have observed the points mentioned above with your company, you must confront the question at the beginning of whether your UK company (Ltd, LLP, or Sole Trader) is transferring an economic asset to the newly founded Maltese company. Because then the Maltese company must pay the UK company for this! Even if it is an intangible asset that you might not even be aware of. And then it means:

This transfer of economic assets must be taxed in the UK. But what are possible economic assets? Here are some examples.

The Malta Limited has…

- Received customers from the UK company.

- Access to the professional network

- Access to the internal CRM system

- Access to suppliers

- Access to staff

- Access to resources

- Access to a business opportunity that generates profit

These are all economic assets that must be taxed in the UK if transferred to the Maltese company.

Rightly, the question arises: What do I have to charge for one point or another?

Well—my favourite sentence—that varies from case to case.

It certainly makes sense to handle this point right at the start of the incorporation. Proactive behaviour is welcomed, and if argued and presented correctly, you should soon have peace of mind on this topic.

I strongly advise you to take action early here! If you give the tax authorities the opportunity to approach you after a few years—and that is quite common—you face a rude awakening.

If the Maltese company has experienced a significant and unexpected increase in value, for example through expansion, it can get expensive. In the worst case, the tax office proceeds by taking the average profit of the past three years as the basis for its calculations.

Often, large parts of the profit must then be taxed retrospectively in the UK, as the basic assumption is made that these profits were only possible through the transfer of economic assets from the UK company. So be careful!

This topic can also be picked up by HMRC over time. If you have clearly defined and reported all interconnections right at the beginning, you have nothing to fear.

6. Transfer of Functions to Malta

If you relocate healthy or functioning parts of your company to Malta, for example purchasing, sales, marketing, or similar, you may have to tax the future profit forecasts of this function in the UK.

Even if the specific laws vary, the topic is gaining importance, especially in times when companies are becoming increasingly mobile.

By the way: Duplicating the function is rather uncritical. But: You won't be able to achieve tax optimization with that.

7. Transfer Pricing Guidelines

Have you ever heard of the "Arm's Length" principle? This principle states that for intra-group (as well as related company) transactions, market prices must always be applied that would stand up to a third-party comparison.

This is a topic not to be underestimated. Depending on the volume of the transaction, the topic goes so far that exactly how transfer prices are composed must be documented according to rules in the form of "Transfer Pricing Documentation".

The methods common here have, by the way, been tightened since the BEPS (Base Erosion and Profit Shifting) financial agreement.

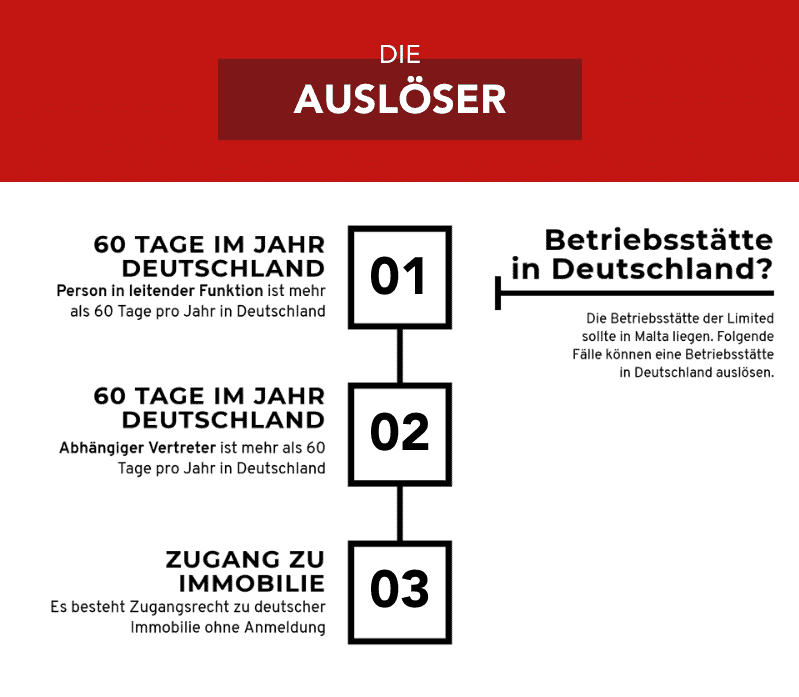

8. Triggering a Permanent Establishment Outside Malta

Even if this point applies not exclusively to a Malta Limited with a UK shareholder, it is still important:

If you keep your residence in the UK, you run the risk of triggering a Permanent Establishment (PE) there for the company in Malta.

Besides the obvious points like a UK office, a branch in the UK, or similar, which all trigger a PE there, there are less obvious points. Fulfilling just one of the mentioned points is enough to trigger a PE in the UK:

9. Value Creation Must Take Place in Malta

There are some companies that are so profitable that they can easily afford the expenses for creating substance in Malta. So it doesn't matter if the director earns a good monthly salary, a decent office is rented, and two full-time employees are employed there.

You might have guessed it, but:

Merely fulfilling the measures mentioned above is not enough for the authorities.

If you run fancy offices in Malta with expensive employees who just twiddle their thumbs there, you will sooner or later attract attention. Because:

It is important that genuine value creation also comes from the staff in Malta. The buzzwords for this are "Key Value Drivers" and "Key Values".

This means that preparatory or administrative activities in Malta are certainly possible, but these are not taken into account for the taxation of the entire company, as these are not the key activities for value creation.

A concise sentence on this: In modern, attributing international tax law, the place of value creation is just as important as the place of the physical permanent establishment. Both must be in Malta.

10. The Role of the Shareholder Residing in the UK

To make it short: Passive is the important word in connection with the role of the shareholder with UK residence.

Compare yourself to the shareholder of a PLC. Although they have certain influence through the shareholders' meeting and must be involved in important decisions, but:

Participating actively and operationally in day-to-day business is not intended. So that should be avoided.

I consciously say "avoided" in this context. Why? Well, of course you can become active yourself, just expect that this part of the business, in which you yourself regularly intervene actively, will be subject to UK taxation.

Interim Conclusion

- Commercially speaking, you are right in assuming that observing the points mentioned above is cost-intensive.

- Administratively speaking, you are right in assuming that observing the points mentioned above means considerable mental effort.

- Emotionally speaking, you are right in assuming that observing the points mentioned above can lead to considerable stress, out of worry about possible conflicts with HMRC.

Therefore, one can at least allow oneself the consideration of leaving the UK and choosing Malta as a residence instead.

Because then the world looks completely different.

Limited Shareholder with Residence in Malta – What Applies Then

Now the question is:

What changes with a residence in Malta?

Quite a lot, I can reveal that much in advance.

Let's start.

Let's get to the comparison:

What does the whole thing look like if the shareholder of the company in Malta decides to pitch their tent in Malta?

You might have guessed it, but here too there are protective mechanisms in tax law intended to prevent the migration of taxpayers.

However, for me, it applies again here: I can understand the government.

Economic successes, which are now obviously no longer available for taxation, are partly built on the UK's infrastructure, education, security, freedom, and self-determination.

Therefore: The fact that a state wants to tax someone leaving one last time is, in my eyes, at least not extraordinary.

Exit Tax / Capital Gains on Leaving

Unlike Germany, the UK does not currently have a general "exit tax" on unrealised capital gains for individuals leaving the country (though this is a topic of constant political debate). However, there are rules regarding Temporary Non-Residence.

If you leave the UK and return within 5 years, certain gains realized while you were away (like selling your company shares) might be taxed in the UK upon your return. This is to prevent people from leaving just to sell an asset tax-free and then coming back.

Also, if you have been a long-term resident, you need to ensure you properly break your tax residence under the Statutory Residence Test (SRT).

Generally speaking: Moving to Malta can be a "Safe Haven", but we advise on a case-by-case basis. There are certainly cases where this makes no sense.

In short: The simplest way is certainly if you are a sole trader when you leave and do not hold shares in other limited companies, or if you plan to leave for the long term (more than 5 years).

Maintaining Ties to the UK

Even if you move to Malta, you must be careful not to accidentally remain a UK tax resident. The UK uses the Statutory Residence Test, which looks at how many days you spend in the UK and how many "ties" (family, accommodation, work) you have there.

If you keep a home available in the UK and visit too often, you might remain tax resident on your worldwide income.

However, unlike some other countries, the UK does not tax based on citizenship. Once you are non-resident, you generally only pay UK tax on UK-sourced income.

Substance is Negligible with Residence in Malta

The most important statement of this article in connection with a residence in Malta:

The long list of requirements for substance does not apply to you then! Most points can be ignored, quite simply because you are no longer a UK taxpayer and accordingly these laws no longer apply.

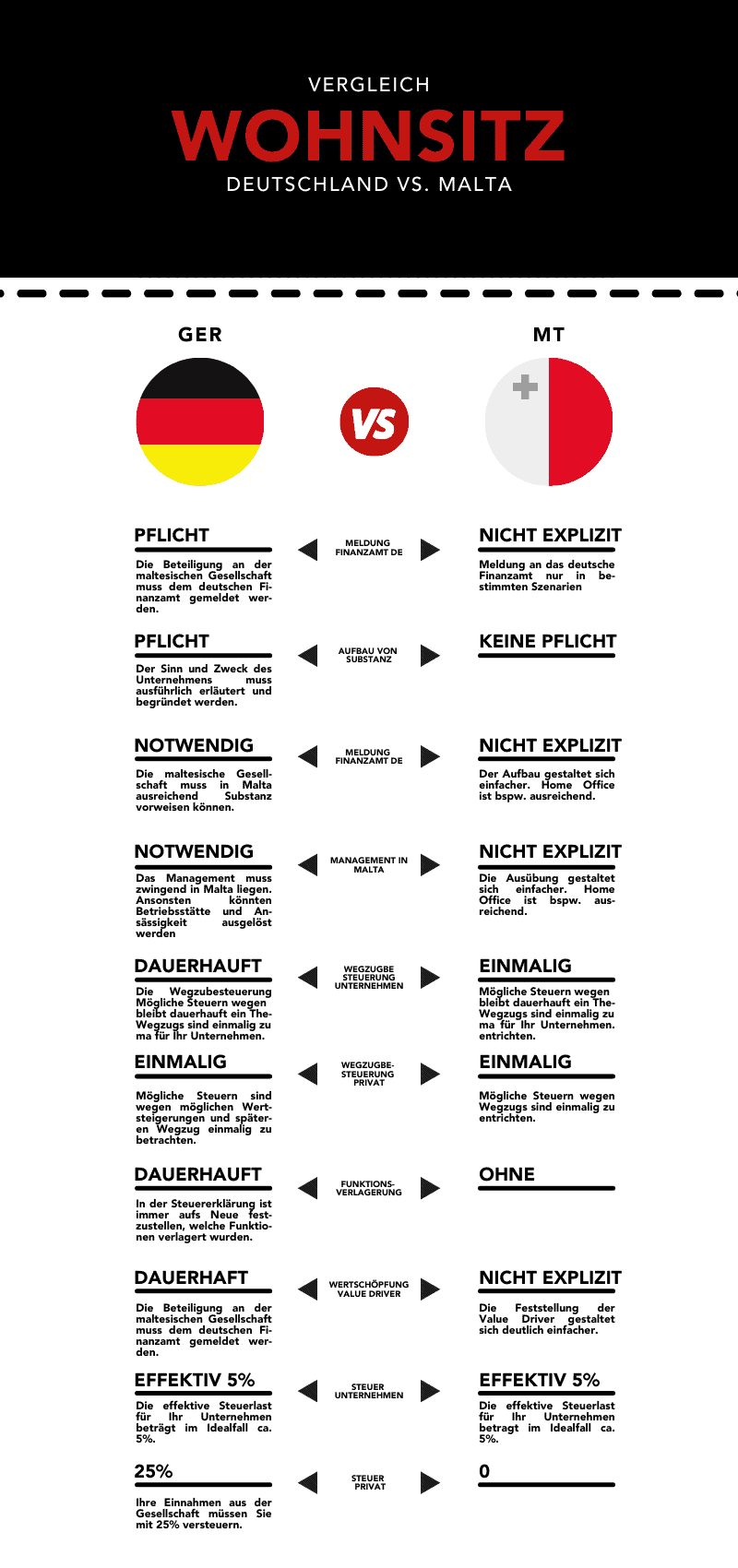

Finally, I would like to compare once again what consequences follow from which residence:

Disclaimer: The content of this article is for general information purposes only and does not constitute tax, legal or financial advice. Despite careful research, we make no guarantee for the accuracy, completeness and timeliness of the information provided. Tax regulations are subject to constant change. For individual advice, please consult a qualified tax advisor. Use of the content is at your own risk.

Stay Informed

Receive our latest articles on international tax planning, relocation and company formation directly in your inbox.

No spam. Unsubscribe anytime.