Banking in Malta 2026 – Facts and Commentary

Last updated: 10 February 2026

Everything You Need to Know About Corporate Accounts, Private Accounts, and Banks in Malta

The first time I walked into a bank in Malta was back in 2009.

It was also my very first time on the island. The unique beauty of the place, especially the image of Valletta's historic old town, remains one of my fondest memories to this day.

Golden sandstone gorges with a legendary patina. Narrow streets forming shaded canyons leading down towards the coast. In the distance, you could sense the deep blue sea, flashing silver here and there.

But I hadn't come from London for sightseeing; I was there to meet a client. The plan was to incorporate a company in Malta and open a business bank account.

All in one day.

What seems unthinkable today (more on that later) was already considered impossible in London back then. But at that time, nobody really had Malta on their radar.

We went to the HSBC branch in Birzebbuga, right in the south of the island. No appointment. Fifteen minutes later, we walked out with an IBAN and a security token for online banking.

Unbelievable. I can tell you this much right now: It is not like that anymore. Over the years, Malta became a victim of its own success.

Today, the banks tick differently. But why is that? What has changed? What is the current state of the banking system in Malta? I'll try to give you an overview. I will also dedicate a chapter to explaining how to actually open a business account for a Malta Limited today.

HSBC Corporate Accounts: A Different World

Today, as an "average Joe," it is simply no longer possible to get an account with HSBC Malta. They only touch the very big players now. We're talking Commercial Banking, turnover of €2.5 million and upwards.

Business Clients in Malta: International vs. National

A local Maltese person doesn't have the problems I'm about to describe. A carpenter from Mosta can still walk into HSBC. Perhaps even without an appointment.

The banks have segmented their clients. As soon as a "foreigner" or a "business case with an international focus" comes into play, the local branch is no longer responsible. Instead, you are passed on to an "International Business Centre."

Being a customer there feels like it only comes with downsides.

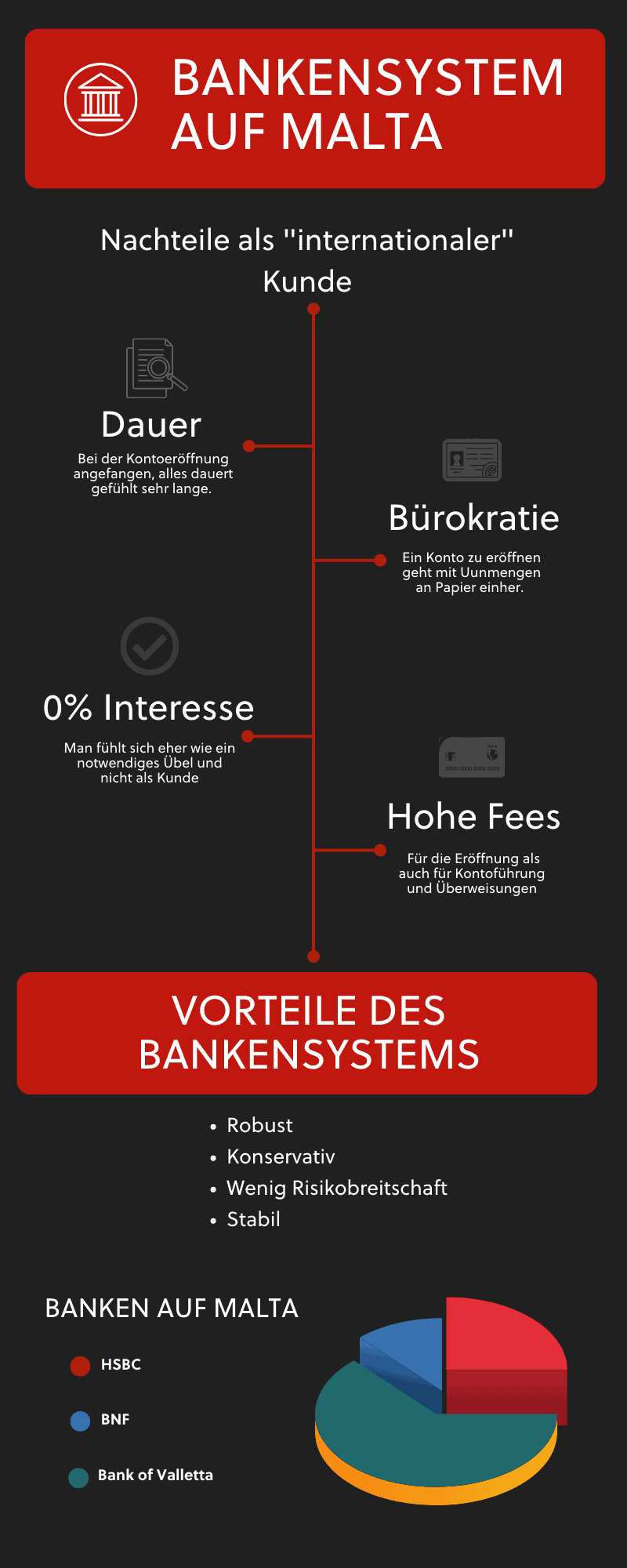

The Disadvantages for Non-Maltese Clients

- Everything takes a long time.

- Everything is questioned.

- There is no credit.

- It is expensive.

- You face unannounced checks.

When I say there is no credit, I'm not talking about quick bridging finance, a standard business loan, or an overdraft facility. I mean there isn't even a simple credit card. Well, they exist, but you often have to deposit double the credit limit as cash collateral.

Double.

I'll get to private clients in a moment, but let me explain why banks in Malta behave the way they do.

Banks in Malta: They Are Doing Too Well

To put it bluntly: they are doing far too well.

There is one business sector that eclipses most other commercial interests, which is why banks have no interest in "small fry."

That sector is:

Servicing the booming Maltese real estate market with mortgages.

And honestly, who can blame them? Banks hate risk. And international "normal" corporate business—with payments coming in and going out across borders—comes with high risk.

Risk?

You might ask, quite rightly. I just wrote above that the bank gives you nothing, especially no credit. So where is the risk?

True, there is no credit default risk. But there is a massive block of other risks:

The Risks for Maltese Banks with International Clients

- Money laundering risk.

- Extremely high fines from the FIAU (Financial Intelligence Analysis Unit) if money laundering is detected.

- Reputational risk in the event of a scandal.

- Cost of compliance to prevent money laundering.

- Cost of adhering to all regulatory requirements.

- Cost of servicing business clients properly.

The official answer for rejecting an international client is usually:

"It is beyond the bank's risk appetite."

By contrast:

The mortgage business with private clients is simple and quiet.

And if something goes wrong, the bank can repossess the house. Consequently, real estate financing is more in demand than ever, meaning banks can pick and choose if and whom they accept as business clients.

But there's a catch.

Fortunately, there are Neo-banks. They have realised that with good technology, the risk is actually quite manageable. These banks don't finance real estate; they focus exclusively on payments.

Neo-banks include Wise, Revolut, N26, Monzo, and so on.

Private Banking for Individuals in Malta

What about personal accounts?

You might laugh.

It actually required executive intervention from the Maltese government to force banks to open at least a "normal" payment account with a debit card for anyone residing in Malta.

The financial regulator, the MFSA, practically ordered the banks to do it: https://www.mfsa.mt/service-detail/payment-accounts-with-basic-features/

Why? Because the banks wanted to be just as fussy with private individuals as they are with companies.

That is at least a glimmer of hope.

Nevertheless, if you have a bit of money, and especially a regular income, it is possible to get an account at a "traditional" bank.

But even here, I find myself asking: Why? Do you really need a local Maltese bank account if you have a simple use case—receiving funds, paying bills, and withdrawing cash from an ATM now and then?

The answer is no.

But—and this is the big "but":

Perhaps you want to buy a house or an apartment in Malta someday. In that case, there is no way around a Maltese bank. Only a local bank can help you with a mortgage for a property in Malta.

Therefore:

Who Are the Main Banks in Malta?

BOV – Bank of Valletta – The Largest Bank

This is the biggest bank on the island. To put its size into perspective:

Net income €199.6m (2024) | Total assets €15.1bn (2024) | Employees: approx. 1,900

Compare that to Deutsche Bank: Net income €5.7bn (2022) | Total assets €1.337 trillion (Q4 2022) | Employees: 84,930 (Q4 2022)

BOV is tiny compared to a major international bank. The Maltese government owns 25% of BOV.

International Business Clients: Accepted, but only with an "Introducer," which adds costs to the opening process. Expect to pay around €2,500 for such an introduction.

An Introducer is a "business facilitator" approved by the bank. The banks choose who they accept as Introducers. For example, with BOV: There are hundreds of law firms and corporate service providers in Malta. BOV currently has only about 25 approved Introducers.

Private Clients: Accepted as "normal" customers if you have a Malta ID card. However, it still involves a lot of paperwork.

HSBC – Only for Corporate Giants

HSBC is in Malta primarily due to the island's British history. The "Midland Bank," back then a small international bank but the largest in Malta, was bought globally by HSBC. Midland disappeared and became HSBC Malta. HSBC likes to boast about being incredibly international while still feeling like "one" bank.

That might be true in other countries.

But in Malta, you are a client of HSBC Malta. Even if you come with the best recommendations from HSBC UK, it gives you zero advantage here.

International Business Clients: Only accepted above a very high turnover threshold.

Private Clients: Accepted with a Malta ID. But again, expect a lot of hassle.

APS – The Church Bank

The "Church Bank," so to speak. APS is indeed owned by the Archdiocese of Malta (approx. 55% via AROM Holdings) and the Diocese of Gozo (approx. 12.5%). The Church is the majority shareholder, but has been gradually reducing its stake since 2022. APS is listed on the Malta Stock Exchange.

Be that as it may:

There aren't significantly more or fewer crucifixes on the walls than in other banks.

International Business Clients: Only accepted with specific "Low Risk" business cases.

Private Clients: Accepted with a Malta ID. Still involves significant effort.

BNF – Post-Crisis Evolution

BNF Bank used to be called BANIF Bank. BANIF was a major Portuguese bank that suffered heavily during the 2008 financial crisis. Part of the subsequent bailout agreement by the Portuguese government was that Banif had to sell the "crown jewels" in its portfolio.

One of those crown jewels was BANIF Bank in Malta.

It was bought by the Qatar-based Al Faisal Holding Group and renamed BNF.

International Business Clients: Only accepted with specific "Low Risk" business cases. High opening fees, high maintenance fees, and high transfer costs.

Private Clients: Accepted with a Malta ID. Significant effort required.

SPARKASSE: Malta Bank with a German Name

Sparkasse in Malta is owned by the Austrian Anteilsverwaltungssparkasse Schwaz (AVS), which also owns Sparkasse Schwaz AG in Tyrol. Through the Austrian savings bank network, it is connected to Erste Group. Sparkasse is too small to have a dedicated International Clients Centre, but they do process niche industries, including gambling clients.

International Business Clients: Accepted, but only with an "Introducer." Expect opening costs of around €2,500.

Private Clients: Accepted with a Malta ID. Significant effort required.

Opening an Account After Incorporation: How It Works

In this chapter, I'll focus on the process rather than the minute details.

Business Account at a Traditional Maltese Bank

Prepare yourself for paperwork and costs. First, you need to hire an Introducer. They will recommend which bank is most suitable for your specific business case.

Then you are "introduced," meaning the application is filed.

A "Bank Introduction" is exactly that: An introduction. Nothing more, nothing less.

An Introducer can give you no guarantee that the bank will actually open the account.

The Introducer and the bank fees usually have to be paid even if the account is refused. The work lies in the application itself. And the bank only decides AFTER reviewing a complete application.

The application is almost always paper-based and asks for endless details about you and your business.

Duration: 1 to 3 months.

Business Account at a Neo-bank for a Malta Limited

Here, you also need a form of introduction, but not from the bank's side. You start the application yourself online on the Neo-bank's website. You might need an advisor to help prepare the information and documents, as Neo-banks also have strict compliance requirements.

However, a Neo-bank will generally not charge fees just for the opening process itself.

The big advantage: It's fast.

Duration: 1 day to 2 weeks.

Buying Property in Malta with a Maltese Bank

If you are thinking about buying real estate in Malta, prepare for comparatively high interest rates. You are likely looking at over 3% p.a. for a mortgage.

More importantly:

The interest rate usually cannot be fixed for long periods, so it is quite possible that you will pay significantly more interest down the line.

Mortgage Financing is generally offered by banks against a 10% deposit.

Of course, this depends entirely on the bank and your profile.

It is much easier:

To get a home loan if you are NOT self-employed. The documents required from a self-employed individual are extensive.

The Myth of the Bank-Financed Property Bubble

You read this from time to time. That the property market is overheated. That everything is too expensive and will collapse "soon." That might be true, and I do think there is a bubble.

But it's not a credit bubble. The property market isn't booming because of loose lending.

The banks do not give mortgages to just anyone; they check exactly who gets a loan.

No, the bubble I see in Malta is a "Tax Bubble."

Why There Is No Credit Bubble

The only reason why:

- Real estate prices are as high as they are, and

- There is high demand from wealthy clients,

...is the low tax.

This applies to both Maltese locals and foreign clients. Both profit from the low tax environment.

How do they profit?

Foreigners profit directly by paying low tax and financing a property.

Maltese locals profit by financing properties to rent them out. They rent to people who have come to Malta because of the low tax.

Or they rent to people who work for someone who came to Malta because of the low tax.

This means:

If, for any reason, taxes in Malta rise, I expect there could be a crash. Property prices would fall, and people with mortgages would be asked by the banks to increase their collateral because the property no longer holds the same value as security.

Conclusion

I am not satisfied with the banking sector in Malta, and I think that comes across clearly in this article. Banks in Malta are selective, expensive, and bureaucratic. They are not competitive with Neo-banks. But I'm not just bashing them for the sake of it; I can understand the banks. The business environment simply dictates this behaviour.

Therefore, my recommendation, especially for the start, is:

If you need to move quickly, open an account with a Neo-bank. In step 2, with less time pressure, you can decide to apply for an account with a traditional bank.

Disclaimer: The content of this article is for general information purposes only and does not constitute tax, legal or financial advice. Despite careful research, we make no guarantee for the accuracy, completeness and timeliness of the information provided. Tax regulations are subject to constant change. For individual advice, please consult a qualified tax advisor. Use of the content is at your own risk.

Stay Informed

Receive our latest articles on international tax planning, relocation and company formation directly in your inbox.

No spam. Unsubscribe anytime.